Chargeback Management Services - Dispute Response Apr/ 3/ 2026 | 0

In the United States, moving money electronically is the lifeblood of commerce. The ACH (Automated Clearing House) network is a massive financial engine that moves tens of trillions of dollars across billions of transactions every single year. For U.S. businesses, ACH payments are a highly attractive option because they transfer funds directly between bank accounts, typically taking just a few business days to process, and they come with significantly lower processing fees than standard credit card transactions.

While credit card fees generally range from 1.5% to 3.5% per transaction, ACH transfers usually cost a fraction of that, making them an incredibly cost-effective solution for recurring billing, high-value invoices, and payroll. However, accessing this network requires partnering with a provider. The landscape of ach payment processing companies is vast, and knowing the different types of providers available is crucial for selecting the right fit for your operational needs.

Here is a breakdown of the different types of ACH providers available to U.S. businesses today.

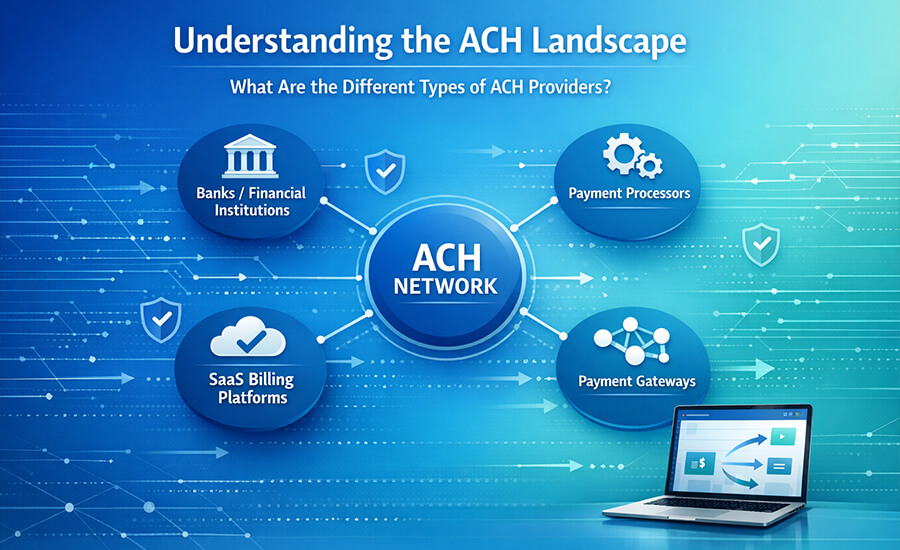

1. Direct Financial Institutions (ODFIs)

At the core of the ACH network are the banks themselves. An Originating Depository Financial Institution (ODFI) is a bank that has an agreement with an ACH Operator to transmit payment entries directly into the network. To originate ACH transactions, a business can establish a direct relationship with an ODFI, which then takes on the responsibility of ensuring all compliance, data security, and authorization rules are met.

While going straight to the source cuts out the middleman, building direct bank integrations can be expensive, highly technical, and time-consuming for the average business to maintain.

2. Third-Party Senders (TPS) and Payment Service Providers

Because integrating directly with an ODFI is complex, many businesses use a Third-Party Sender (TPS) or a Third-Party Service Provider. A TPS acts on behalf of your business (the Originator) by maintaining a contractual relationship with an ODFI to transmit entries. In this arrangement, your business does not need a direct agreement with the bank.

These providers typically offer user-friendly dashboards, pre-built templates, and streamlined customer support to make accepting ACH payments much easier for standard small-to-medium businesses. They bridge the technical gap, making affordable ACH processing accessible to everyday merchants.

3. API-First and Developer-Focused Platforms

For businesses with high transaction volumes, manual data entry is impossible. API-driven ACH providers specialize in software integrations that automate payments at massive scale. These ach payment processing companies provide Application Programming Interfaces (APIs) that allow your proprietary software to communicate directly with the ACH network.

If you manage a digital marketplace, property management software, or a high-volume B2B platform, API-focused providers are ideal. They allow you to write code that automatically initiates thousands of transactions, handles mass payouts, and seamlessly manages digital wallets without requiring manual intervention.

4. Subscription and B2B Automation Specialists

Some providers heavily tailor their services toward specific business models, such as recurring subscriptions or B2B invoicing. These providers automate accounts payable and receivable, offer automated invoice matching, and establish sophisticated approval workflows. For businesses relying on direct debit for monthly memberships, software-as-a-service (SaaS) fees, or routine vendor payouts, these specialized platforms significantly reduce payment failures and eliminate manual invoicing.

5. High-Risk Merchant Account Providers

Not all businesses easily qualify for standard payment processing. A business is typically classified as “high risk” if it has unpredictable revenue, operates in a heavily regulated industry, or sustains a chargeback ratio above 1%. Businesses that have previously had their accounts terminated and placed on an industry MATCH list also fall into this category.

High-risk ACH providers specialize in securing processing capabilities for these hard-to-place merchants. They offer flexible underwriting, specialized risk management tools, and hands-on support to help businesses maintain stable payment processing despite elevated industry risks.

Protecting Your Revenue with Dispute Response

Regardless of which of the many ach payment processing companies you choose to power your business, you will inevitably face the complexities of returned payments. ACH transactions can be returned for nearly 70 different reasons, including insufficient funds, incorrect banking details, or unauthorized transaction claims. Furthermore, instances of business email compromise and payment fraud are persistent threats that can lead to costly unauthorized returns.

This is where Dispute Response becomes an invaluable partner.

Dispute Response is dedicated to helping U.S. businesses expertly navigate the headaches of ACH returns, chargebacks, and payment disputes. Managing risk and fighting invalid disputes takes away valuable time from running your operations. At Dispute Response, we specialize in tackling the heavy lifting of dispute mitigation and resolution. We work alongside your existing payment infrastructure to ensure that when a dispute or return threatens your bottom line, you have a professional, rapid-response strategy in place to recover your funds and protect your merchant standing.

Whether you process payments through an API gateway, a high-risk provider, or a traditional Third-Party Sender, Dispute Response empowers you to keep your focus on scaling your business while we expertly handle the rest.