Chargeback Management Services - Dispute Response Oct/ 18/ 2025 | 0

In 2025, managing chargebacks is a critical part of ensuring business continuity, especially for merchants in high-risk sectors. One of the tools businesses use to protect themselves financially from chargeback risks is reserve funds. But how do these funds work, and how does effective chargeback management contribute to your business’s long-term success? In this blog, we’ll dive into the details of reserve funds and how integrating strong chargeback management practices can help safeguard your business.

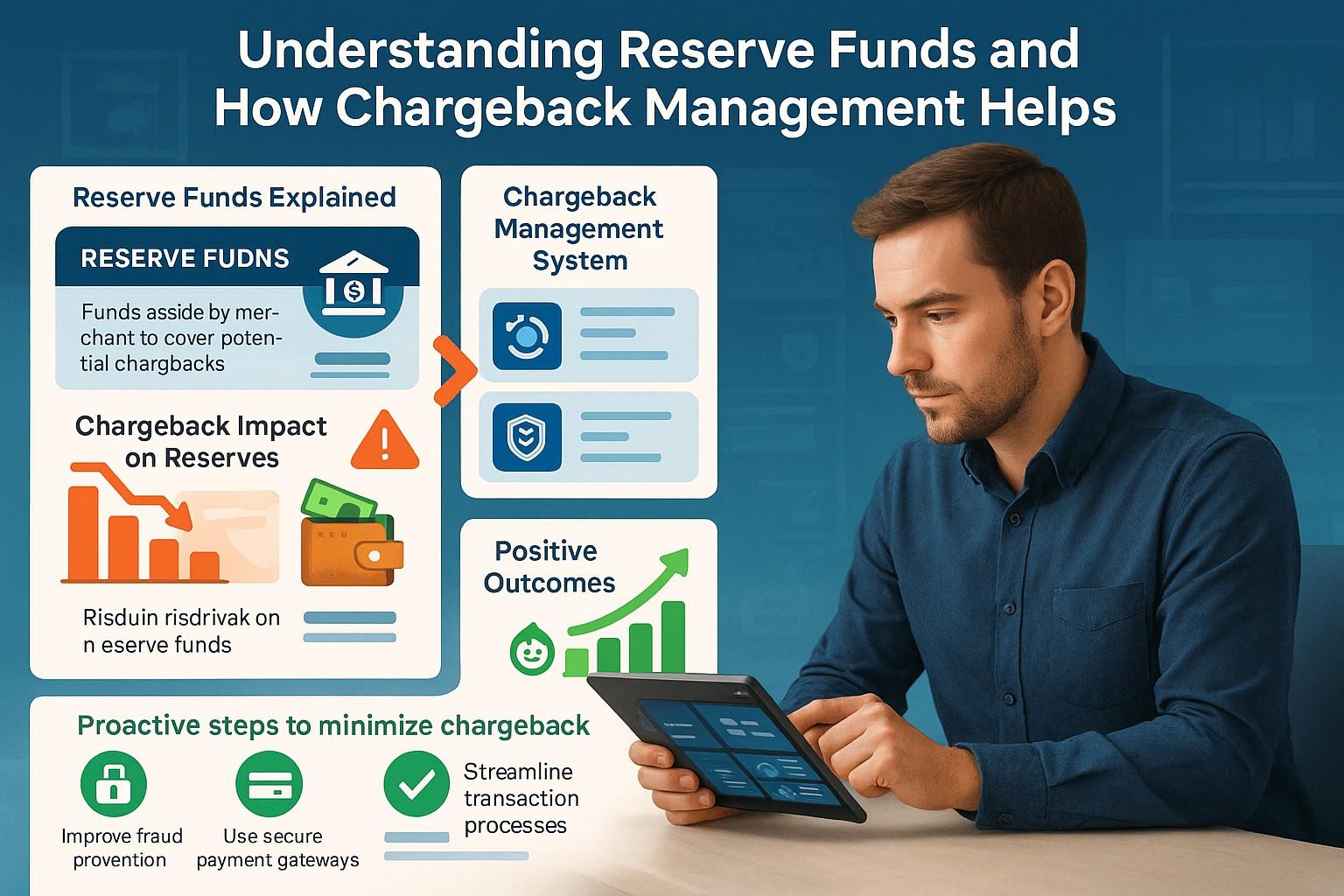

What Are Reserve Funds?

A reserve fund is a percentage of your business’s transaction volume that is held by a payment processor or financial institution. This fund serves as a security buffer to cover potential chargebacks, fraud, or refunds. The reserve is typically withheld from the merchant’s payout and can either be held for a set period or until the merchant’s account proves a consistent history of low chargeback rates.

Types of Reserve Funds

There are two common types of reserve funds:

- Rolling Reserve: A percentage of your sales is held for a period (usually 30 to 180 days) to cover future chargebacks. Once the period ends, funds are released.

- Fixed Reserve: A fixed amount of funds is held and is not tied to sales performance. This reserve provides a more predictable safety net.

How Does Chargeback Management Help?

Chargebacks are one of the most significant risks merchants face, especially in industries prone to disputes and fraud. Effective chargeback management helps businesses reduce the likelihood of chargebacks, thus reducing the need for large reserve funds.

Here’s how chargeback management works to benefit your business:

1. Reducing Chargeback Rates

A well-structured chargeback management strategy can minimize your chargeback rate by identifying and addressing the root causes of disputes, whether it’s fraud, customer dissatisfaction, or transaction errors.

2. Improving Customer Relationships

By addressing disputes quickly and professionally, you can improve customer satisfaction and prevent future chargebacks, ensuring that customers feel heard and valued.

3. Optimizing Financial Flow

Lower chargeback rates mean less money tied up in reserves, giving your business more flexibility and improved cash flow.

4. Enhancing Fraud Prevention

A proactive approach to chargeback management includes tools like fraud detection and real-time alerts, allowing you to stop fraudulent transactions before they impact your bottom line.

How to Manage Reserve Funds Effectively

Though reserve funds are designed to protect businesses, they can also tie up significant amounts of capital. Here are some tips for managing reserve funds effectively:

- Maintain Low Chargeback Ratios: The key to reducing your reserve funds is maintaining a low chargeback ratio. Work on strengthening fraud prevention techniques, providing clear billing descriptors, and responding promptly to disputes.

- Work with Your Payment Processor: Stay in close communication with your payment processor to negotiate lower reserves or find opportunities to reduce reserve amounts as your business proves its reliability.

Email us anytime!

Email customer service 24/7

Call us anytime!

Reach customer care 24/7 at +1 (888) 927-5152

Conclusion

Reserve funds are an essential tool for safeguarding your business against chargebacks, but managing them effectively requires more than just holding funds in reserve. By integrating solid chargeback management practices, businesses can reduce chargeback rates, lower the need for large reserves, and improve overall financial health.

For businesses looking to optimize their chargeback management in 2025, partnering with a chargeback management firm can make all the difference. Start implementing better practices today to reduce your chargeback risks and take control of your reserve funds.