Chargeback Management Services - Dispute Response Mar/ 27/ 2026 | 0

It happens to the best of us. You check your checking account and realize a scheduled bill is about to pull more money than it should—perhaps $1,000 instead of the $100 you expected. Or maybe an unfamiliar company is about to debit your account without your permission. In a panic, you immediately reach out to your financial institution to issue a stop payment.

But does an ACH stop payment post immediately? And more importantly, will it actually stop the funds from leaving your account?

At Dispute Response, we help consumers across the USA navigate the confusing world of banking errors, disputes, and unauthorized transactions. Let’s dive into how stop payments work on the automated clearing house network and what you can do to protect your hard-earned money.

Understanding the Automated Clearing House Network

First, it is helpful to understand how these payments operate behind the scenes. ACH stands for the automated clearing house, which is an electronic processing network used to handle bank-to-bank transfers in the United States. It is the system responsible for your direct deposits, payroll, and automatic monthly bill payments.

Unlike expensive wire transfers that process in real-time, traditional transfers on the automated clearing house network are processed in batches and can take one to three business days to fully settle. However, the banking landscape is evolving. With the rise of same-day processing capabilities, funds can now be moved and settled within a matter of hours.

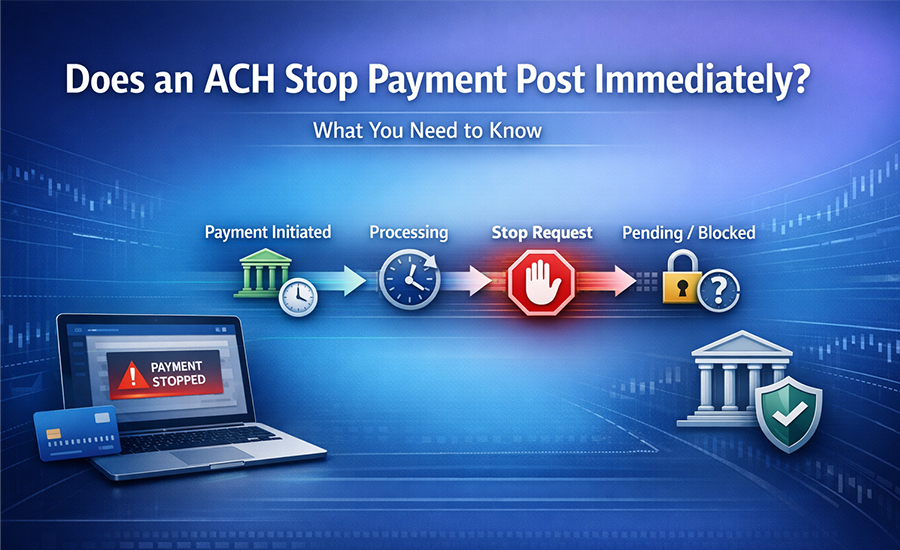

Do Stop Payments Take Effect Instantly?

The short answer is: while your bank may log your request immediately, it does not mean the payment is instantly or permanently blocked. Because the automated clearing house system relies on specific daily processing windows, timing is absolutely critical.

If you are trying to stop a recurring payment, federal regulations generally require you to notify your financial institution at least three business days before the expected transfer date. If you request a stop payment within that three-day window, your bank will usually make a “best effort” to halt the transaction, but they are generally not held liable if sufficient time was not provided and the payment slips through.

Furthermore, you must be aware that a stop payment order is not always permanent. Often, a verbal request made over the phone is only binding for 14 calendar days. If you do not follow up with a written confirmation within that 14-day period, the stop payment will expire, and the merchant can successfully pull the funds. Even a written stop payment order typically expires after six months unless you proactively renew it.

Why Do Stop Payments Sometimes Fail?

You might do everything by the book, contact your bank early, and still wake up to find your account overdrawn. Here are common reasons why an ACH stop payment might fail to work:

- Mismatched Information: Financial institutions rely on automated computer systems to catch stopped payments. If the merchant name or the exact dollar amount you provide is off by even a single character or a few cents, the stop payment will likely fail. For instance, if you issue a stop payment for a $35.00 charge to “Company XYZ” but the actual charge comes through as $35.25 from “CompanyXYZ, Inc.”, the transaction could easily bypass the system’s block.

- Same-Day Speed: With modern same-day processing, the window to catch a payment is incredibly compressed. If a merchant initiates a transfer and you try to stop it the same morning, you might miss the banking cutoff times entirely, resulting in the payment settling before the block takes effect.

- Merchant Evasion: In cases of fraud or highly aggressive billing, bad actors frequently change their merchant ID or tweak the transaction amount specifically to get around your stop payment orders.

How to Effectively Stop an Automated Clearing House Payment

To give yourself the best chance of success, Dispute Response recommends following these best practices:

- Revoke Authorization Directly: Your first step should always be to contact the company pulling the funds and formally revoke their authorization to debit your account.

- Contact Your Bank Early: Submit your stop payment order at least three business days before the transaction date to comply with standard banking timeframes.

- Provide Exact Details: Give your bank the precise name of the merchant, your exact account number, and the exact expected transaction amount. Let them know if you want to stop a single transaction, multiple transactions, or all future debits from that specific company.

- Get it in Writing: Always follow up a phone call with a written and signed stop payment form within 14 days to ensure the block remains active.

How Dispute Response Can Help

What happens when you do everything right, but the payment still clears, leaving your account in the negative? Under federal consumer protection laws, U.S. consumers have the right to dispute unauthorized electronic fund transfers. You do not have to accept the loss simply because a bank’s automated system failed to catch a charge.

This is where Dispute Response steps in. Dealing with massive financial institutions can be incredibly frustrating. When you are bounced between automated phone trees or told by a teller that a failed stop payment is your own fault, you need an expert advocate on your side.

At Dispute Response, we specialize in holding financial institutions and dishonest merchants accountable. We understand the complex rules governing the automated clearing house network and know exactly how to leverage consumer protection laws in your favor. If you are struggling to recover funds from an unauthorized transaction or a failed stop payment, Dispute Response is here to help you fight back and reclaim your money.

Don’t let banking errors drain your accounts. Contact Dispute Response today, and let us take the stress out of your financial disputes.