In today’s fast-paced business landscape in the USA, moving money electronically is no longer a luxury—it is an absolute necessity. From paying vendors and collecting subscription fees to ensuring employees receive their wages on time, electronic transfers keep the economy moving. However, if you are managing finances for your business, you have likely come across the terms “ACH” and “direct deposit.”

Because these terms are often used interchangeably, many business owners assume they are completely different systems. Are they the same thing? The short answer is: every direct deposit is an ACH payment, but not every ACH payment is a direct deposit.

To help you optimize your company’s payment operations, let’s break down exactly how these two concepts differ, how they function, and how your business can navigate the occasional disputes that arise during electronic processing.

What is the Automated Clearing House (ACH)?

To understand the differences, we must first look at the broader system. The automated clearing house network is the primary backbone for the electronic movement of money and related data across the United States. It connects virtually every financial institution in the country, allowing businesses and individuals to transfer funds directly between bank accounts efficiently and securely.

Unlike wire transfers that move money individually in real-time, the automated clearing house system processes transactions in bundles or “batches” at scheduled intervals throughout the business day. This batch processing model is what keeps the costs incredibly low compared to other payment methods.

The network facilitates a massive range of transactions, which are categorized into two main types:

- ACH Credits: These are “push” payments where the sender initiates the transaction to push funds from their bank account into the recipient’s account.

- ACH Debits: These are “pull” payments where the recipient (usually a business) requests and pulls funds from the sender’s account, provided they have authorization. This is commonly used for recurring utility bills, auto-pay subscriptions, and B2B vendor payments.

What is a Direct Deposit?

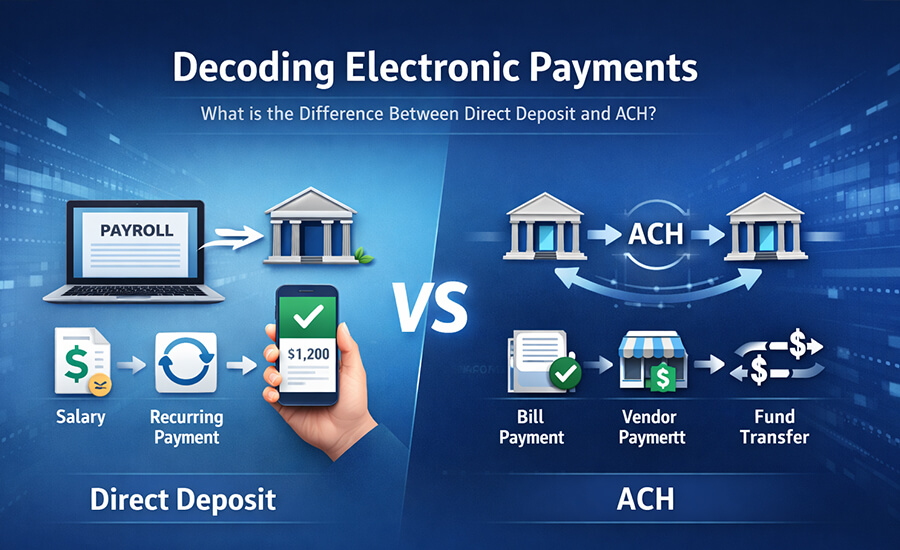

A direct deposit is simply a highly specific type of ACH credit transaction. It strictly involves the electronic transfer of funds directly into a consumer’s checking or savings account.

When a business runs payroll and deposits wages directly into an employee’s bank account instead of handing them a physical paper check, they are utilizing a direct deposit. Beyond corporate payroll, direct deposits are routinely used by government agencies to distribute tax refunds, Social Security benefits, and other social aid.

In short, direct deposit relies entirely on the automated clearing house infrastructure to function, but its scope is limited to crediting an individual’s account.

The Core Differences Summarized

While they rely on the same technological rails, the primary differences lie in how and why they are used:

- Direction of Funds (Credit vs. Debit) This is the most defining difference. ACH payments can be either credits (adding money) or debits (withdrawing money). Direct deposit only ever involves crediting money to a recipient’s account. You cannot use a direct deposit to charge a customer for a service.

- Scope and Usage Direct deposits are reserved for consistent, one-way transfers—most notably employee wages, pensions, and government benefits. ACH, as an umbrella term, covers a vast array of electronic movements. It is heavily utilized for business-to-business (B2B) settlements, accounts receivable, peer-to-person transfers, and recurring consumer billing.

- Processing Timelines Because ACH transactions are processed in batches, they typically take one to three business days to fully clear and settle. A direct deposit, however, is scheduled in advance by an employer’s payroll system. This ensures that the funds clear and are fully available to the employee precisely on their designated payday.

Navigating Payment Exceptions and Disputes

Both of these electronic transfer methods are incredibly secure, heavily encrypted, and tightly regulated by laws such as the Electronic Fund Transfer Act. However, no system is entirely immune to errors, misunderstandings, or complications.

Because the automated clearing house network facilitates ACH debits (pulling money from customer accounts), businesses occasionally run into roadblocks. A transaction might bounce back due to insufficient funds, a closed account, or a mistyped routing number. More significantly, a consumer might claim they did not authorize a transaction or that a recurring billing date was incorrect, leading them to file a dispute or a stop-payment order with their bank. When this happens, the funds are returned, and your business takes a hit.

Managing these electronic payment disputes, tracking down return codes, and proving authorization can be an administrative nightmare that drains your team’s time and impacts your cash flow.

This is exactly where Dispute Response becomes your ultimate business partner.

At Dispute Response, we specialize in helping USA-based businesses effortlessly navigate and resolve electronic transaction disputes. We understand that dealing with unauthorized ACH returns and complex compliance regulations takes you away from what you do best—growing your business. Our tailored services provide you with the tools, expert responses, and streamlined strategies needed to fight invalid chargebacks, manage return codes, and protect your hard-earned revenue.

Conclusion

Understanding the distinction between a direct deposit and an ACH transfer allows you to make more informed choices about your company’s accounts payable and accounts receivable. While direct deposit is the ultimate tool for paying your team, leveraging the full power of the automated clearing house network allows you to automate billing and seamlessly collect revenue.

When exceptions and disputes inevitably arise in your payment processing, you don’t have to face them alone. Let Dispute Response handle the friction of payment disputes so you can focus on scaling your business with confidence.